The Mandatory Provident Fund Schemes (Amendment) Ordinance 2016 (“Amendment Ordinance”) mandates each Mandatory Provident Fund (“MPF”) scheme to provide Default Investment Strategy (“DIS”), with effect from 1 April 2017.

What is the DIS?

DIS is a ready-made MPF investment strategy with fee caps.

For scheme members who do not make any investment choice, their future contributions will be invested according to the DIS.

It is also available for scheme members who find that the strategy suits their own personal circumstances.

What are the main features of DIS?

Feature 1: DIS consists of two constituent funds

The DIS consists of Core Accumulation Fund (“CAF”) and the Age 65 Plus Fund (“A65F”) under each scheme.

The CAF invests 60% of its net asset value in higher risk assets and 40% in lower risk assets, while the A65F invests 20% of its net asset value in higher risk assets and 80% in lower risk assets.

Adopt a globally diversified investment approach with an investment performance standard benchmark for reference.

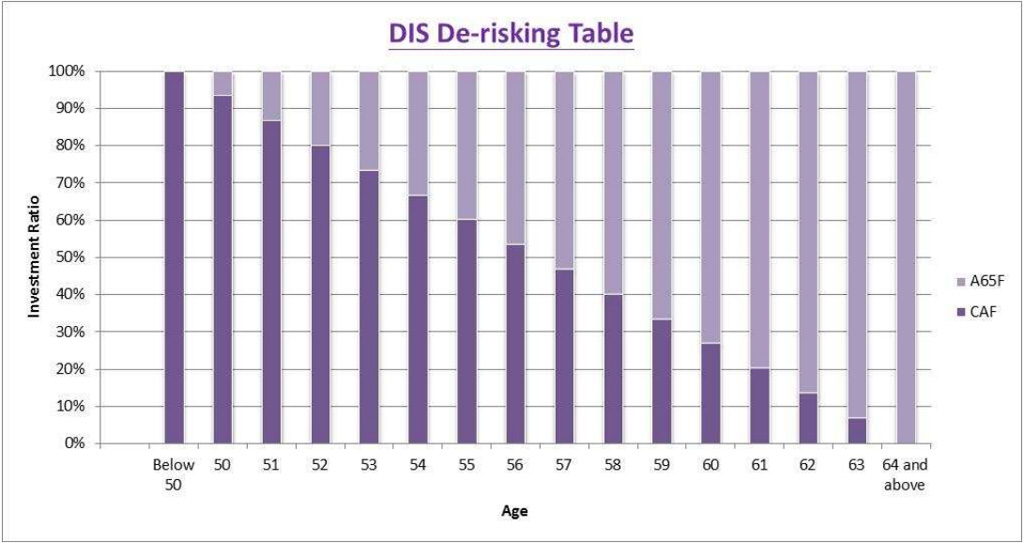

Feature 2: Age-based de-risking mechanism

In order to balance long-term risks and returns, investments will be invested through the predetermined allocation percentages between the two constituent funds in accordance with the member’s age.

Scheme members who invest through the DIS will have all of their contributions invested in the CAF until they reach the age of 50, from which point their investments will be gradually moved to A65F. By the time the members reach age 64, all of their MPF assets will be invested in A65F. Refer to the illustration table as below.

Feature 3: Fee controls

The management fees chargeable to the DIS funds, CAF and A65F, are capped at a maximum of 0.75% of the net asset value of the funds on a yearly basis, while fees for recurrent operational expenses are capped at 0.2% on the same basis.

The management fees covered within the fee cap include all fees for services provided by trustees, administrators, investment managers, custodians, sponsors and promoters, as well as similar fees chargeable to the underlying investment funds.

You should consider your own risk tolerance level and financial circumstances before making any investment choices. In your selection of funds, if you are in doubt as to whether a constituent fund is suitable for you (including whether it is consistent with your investment objectives), you should seek financial and/or professional advice and choose the fund(s) most suitable for you taking into account your circumstances.

Important Note - Fraudulent Websites

BOCI-Prudential Trustee Company (“our Company”) found fraudulent websites which seek to pass off as our Company, and can be searched and accessed through internet search engines. Customers are advised to always stay vigilant about scams.

Please note that www.bocpt.com is the ONLY official website of our Company. We have not authorized any agent or third party to use any of our materials and trademarks to set up other websites. If you have any doubts, please contact our Customer Service Hotlines at 2929-3030/2929-3366 or email to mpf@bocpt.com for verification. Please click here for more security information.

Please read the Terms and Conditions on the Website before using any services available on the website and / or via telephone services (collectively, the “Services”). Your continued use of the Services will mean that you irrevocably and unconditionally accept and agree to be bound by the Terms and Conditions as the same may be amended from time to time and any amendment to the Terms and Conditions shall be effective immediately upon posting on the Website.

BOC-Prudential Easy-Choice Mandatory Provident Fund Scheme

IMPORTANT INFORMATION

You should consider your own risk tolerance level and financial circumstances before making any investment choices. When, in your selection of Constituent Funds, you are in doubt as to whether a certain Constituent Fund is suitable for you (including whether it is consistent with your investment objectives), you should seek financial and/or professional advice and choose the Constituent Fund(s) most suitable for you taking into account your circumstances.

You should consider your own risk tolerance level and financial circumstances before investing in the MPF Default Investment Strategy (as defined in section 6.7 (MPF Default Investment Strategy)). You should note that the BOC-Prudential Core Accumulation Fund and the BOC-Prudential Age 65 Plus Fund may not be suitable for you, and there may be a risk mismatch between the BOC-Prudential Core Accumulation Fund and the BOC-Prudential Age 65 Plus Fund and your risk profile (the resulting portfolio risk may be greater than your risk preference). You should seek financial and/or professional advice if you are in doubt as to whether the MPF Default Investment Strategy is suitable for you, and make the investment decision most suitable for you taking into account your circumstances.

You should note that the implementation of the MPF Default Investment Strategy may have an impact on your MPF investments and accrued benefits. We recommend that you consult with the Trustee if you have doubts on how you are being affected.

Fees and charges of a MPF conservative fund can be deducted from either (i) the assets of the fund or (ii) members’ account by way of unit deduction. The BOC-Prudential MPF Conservative Fund uses method (i) and, therefore, unit prices/NAV/fund performance quoted have incorporated the impact of fees and charges.

If you are in doubt about the meaning or effect of the contents of the information in this website, you should seek independent professional advice.

My Choice Mandatory Provident Fund Scheme

IMPORTANT INFORMATION

You should consider your own risk tolerance level and financial circumstances before making any investment choices. When, in your selection of Constituent Funds, you are in doubt as to whether a certain Constituent Fund is suitable for you (including whether it is consistent with your investment objectives), you should seek financial and/or professional advice and choose the Constituent Fund(s) most suitable for you taking into account your circumstances.

You should consider your own risk tolerance level and financial circumstances before investing in the MPF Default Investment Strategy (as defined in section 6.7 (MPF Default Investment Strategy)). You should note that the My Choice Core Accumulation Fund and the My Choice Age 65 Plus Fund may not be suitable for you, and there may be a risk mismatch between the My Choice Core Accumulation Fund and the My Choice Age 65 Plus Fund and your risk profile (the resulting portfolio risk may be greater than your risk preference). You should seek financial and/or professional advice if you are in doubt as to whether the MPF Default Investment Strategy is suitable for you, and make the investment decision most suitable for you taking into account your circumstances.

You should note that the implementation of the MPF Default Investment Strategy may have an impact on your MPF investments and accrued benefits. We recommend that you consult with the Trustee if you have doubts on how you are being affected.

Fees and charges of a MPF conservative fund can be deducted from either: (i) the assets of the fund; or (ii) members’ account by way of unit deduction. The My Choice MPF Conservative Fund uses method (i) and, therefore, unit prices/NAV/fund performance quoted have incorporated the impact of fees and charges.

If you are in doubt about the meaning or effect of the contents of the information in this website, you should seek independent professional advice.